|

LISTEN TO THIS THE AFRICANA VOICE ARTICLE NOW

Getting your Trinity Audio player ready...

|

Africa is the most mineral-rich continent on earth. That sentence is repeated so often that it has lost its weight. So let’s be specific.

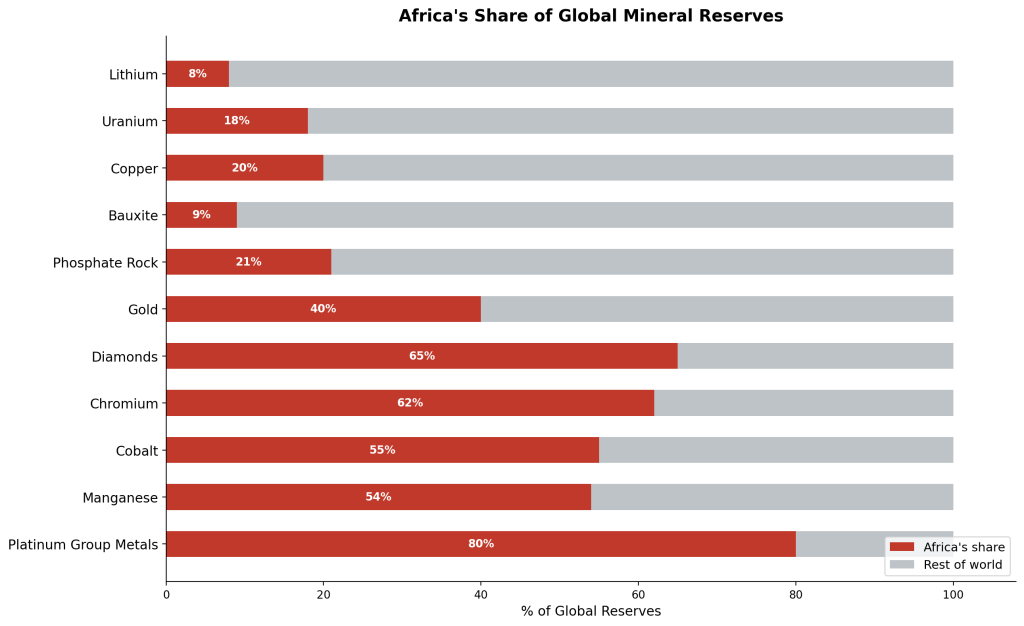

The continent holds 80% of the world’s platinum, 55% of its cobalt, 65% of its diamonds, 40% of its gold, and 54% of its manganese. It sits on an estimated $29.5 trillion in mineral value at mine sites, according to the Africa Finance Corporation’s 2026 Compendium of Africa’s Strategic Minerals. That figure represents roughly 20% of all known mineral wealth on the planet. Of that $29.5 trillion, $8.6 trillion has not yet been touched, equal to about 2.5 times the continent’s annual GDP.

And yet, in 2022, Africa’s total mine production generated an estimated $270 billion in value, a fraction of what the minerals are worth once processed. African countries currently collect only about 40% of potential revenues from their own resources. The continent loses roughly $89 billion annually to illicit financial flows, with the extractives sector heavily implicated. And the International Monetary Fund estimates that sub-Saharan Africa loses an additional $450-$730 million per year in corporate income tax revenue alone due to profit shifting by multinational mining companies.

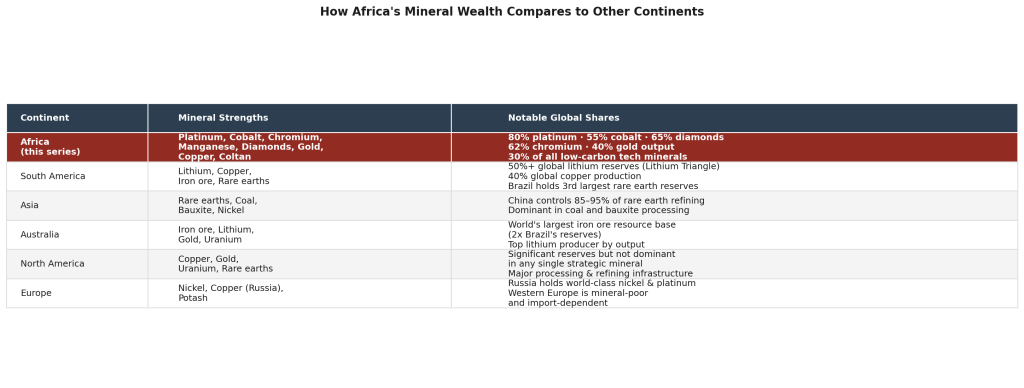

How Africa Stacks Up Against the World

No other continent comes close to Africa in terms of precious and strategic minerals. South America holds the world’s largest lithium reserves, concentrated in the so-called Lithium Triangle of Argentina, Chile, and Bolivia, which together account for more than 50% of known global lithium deposits. The region also produces roughly 40% of global copper, with Chile and Peru as the main producers. Australia dominates iron ore, holding the world’s largest iron ore resource base at more than twice Brazil’s reserves, and is the world’s top lithium producer despite holding smaller reserves than South America. Asia, led by China, controls the rare-earth supply chain, with China accounting for 85-95% of global rare-earth refining capacity. North America and Europe hold significant but comparatively modest mineral reserves across most categories.

Africa, by contrast, dominates the minerals that the 21st century cannot function without. According to the B20 South Africa report on critical minerals, the continent holds approximately 30% of the world’s reserves of minerals essential for low-carbon technologies and digital infrastructure. It leads globally in cobalt (55% of reserves), platinum group metals (80%), chromium (62%), manganese (38% of reserves, 70% of resources), and diamonds (65%). It produces 40% of global gold output, supplies 12% of the world’s oil, and holds 8% of its natural gas.

South America may own the lithium triangle, but the DRC and Zambia together form the cobalt and copper belt that electric vehicles run on. Australia may ship more iron ore, but no continent on earth can match Africa’s combined endowment of the metals that power modern industry, energy systems, and electronics. The cruel irony is that despite holding all of this, Africa attracted only 10.4% of global mineral exploration investment in 2024, down from 16% in 2004, and processes less than 9% of its copper and under 5% of most other key minerals before export. The continent is the world’s most important mineral supplier and its least compensated one.

This is Part 1 of a three-part investigation into who controls Africa’s mineral wealth, how much the continent loses each year, and what the road to ownership looks like. Before we get to the corporations listed on the London Stock Exchange and the political machinery that protects them, you need to know what is actually in the ground.

The Mineral Map: Who Has What

Africa’s mineral wealth is not randomly scattered. It follows geological patterns laid down over hundreds of millions of years, and understanding those patterns is the first step toward understanding why certain countries have been exploited more intensely than others.

Southern Africa: The Platinum and Diamond Belt

The Bushveld Igneous Complex in South Africa is the single most mineralogically significant geological formation on earth. It spans roughly 66,000 square kilometers across three South African provinces and contains an estimated 63,000 metric tonnes of platinum group metals (PGMs), representing approximately 77.8% of all known PGM reserves on the planet. South Africa currently supplies over 70% of global platinum mine output, and the World Platinum Investment Council has confirmed a third consecutive annual supply deficit in 2025. Platinum is essential for catalytic converters in vehicles, hydrogen fuel cells, and a growing array of industrial applications.

Zimbabwe’s Great Dyke, running 550 kilometers from north to south through the center of the country, is the world’s second-largest PGM deposit, ranking third globally after South Africa and Russia.

On diamonds: the Kaapvaal Craton, spanning South Africa, Botswana, Zimbabwe, and Namibia, is the world’s oldest and most diamond-bearing geological province. Botswana alone holds some of the richest kimberlite pipes ever discovered. The Jwaneng mine, operated as a joint venture between the government-owned Debswana and De Beers, is considered the world’s richest diamond mine by value, with De Beers confirming 2025 production guidance of 20 to 23 million carats.

|

Country |

Primary Minerals |

Global Rank / Share |

|

South Africa |

Platinum, Palladium, Gold, Coal, Manganese, Diamonds, Iron ore, Chrome |

World’s largest PGM reserves (77.8%); top global platinum producer |

|

Botswana |

Diamonds, Nickel, Copper, Coal |

Top diamond producer by gem quality; Jwaneng is the world’s richest mine by value |

|

Zimbabwe |

Platinum, Diamonds, Lithium, Gold, Chrome |

3rd largest PGM reserves globally; significant lithium deposits |

|

Namibia |

Diamonds, Uranium, Copper, Zinc |

Top 3 global uranium producers (12% of world supply in 2025) |

|

Zambia |

Copper, Cobalt |

World-class copper; part of the world’s largest copper belt |

Central Africa: The Battery Metals Superpower

The Democratic Republic of Congo is, in the words of economists at the World Bank, a country with “80 million hectares of arable land and over 1,100 minerals and precious metals.” In monetary terms, economists estimate that Congo holds $24 trillion in untapped mineral wealth.

The DRC supplied 76.6% of global mined cobalt output in 2024, producing 220,000 metric tonnes. It ranks as the world’s third-largest copper producer and is also the world’s largest tantalum producer, a metal used in capacitors and electronic components for smartphones, laptops, and aerospace applications. Coltan, a black tar-like ore from which both tantalum and niobium are extracted, is found in major concentrations in the DRC’s eastern provinces of North Kivu, South Kivu, and Maniema.

The DRC’s mineral geography is a direct reason for the country’s political tragedy. The eastern provinces of Katanga, North and South Kivu, Ituri, and Maniema sit on vast deposits of cobalt, copper, tin, tungsten, tantalum, and gold. They are also the provinces that have experienced the most intense armed conflict over the past three decades. The connection is not coincidental.

|

Country |

Primary Minerals |

Key Facts |

|

DRC |

Cobalt, Copper, Coltan, Diamonds, Gold, Tin, Tantalum |

76.6% of global cobalt; $24 trillion total estimated mineral wealth |

|

Zambia |

Copper, Cobalt, Zinc, Lead |

820,000 tonnes of copper produced in 2024; targeting 3 million tonnes by 2035 |

|

Angola |

Diamonds, Oil, Iron ore |

Diamonds are concentrated in Lunda Norte province |

|

Rwanda / Burundi |

Tantalum, Tungsten, Tin, Gold |

Among the world’s top 3T mineral suppliers |

West Africa: The Gold Coast Lives Up to Its Name

West Africa runs along what geologists call the West African Craton and the Birimian Greenstone Belt, a geological formation that produced some of the world’s largest gold deposits. Ghana has reclaimed its title as Africa’s largest gold producer, recording $20 billion in gold export earnings in 2025, nearly double its 2024 total.

Mali, Burkina Faso, and Côte d’Ivoire are substantial gold producers within the same belt. Senegal has emerged as an oil and gas producer. Guinea holds one of the world’s largest bauxite reserves and supplies 95% of Africa’s bauxite output, a critical input for the global aluminum industry. In 2026, Guinea’s first-quarter bauxite output jumped 25% year-over-year, cementing its dominance.

Nigeria’s primary wealth is oil, with 37.28 billion barrels in proven reserves as of 2025. It also holds significant deposits of tin, columbite, iron ore, coal, and tantalite, though its non-oil mining sector remains underdeveloped.

|

Country |

Primary Minerals |

Key Facts |

|

Ghana |

Gold, Bauxite, Manganese, Oil |

$20B in gold exports in 2025; Africa’s top gold producer |

|

Guinea |

Bauxite, Gold, Iron ore, Diamonds |

Holds world-class bauxite; 95% of Africa’s bauxite supply |

|

Mali |

Gold |

Major gold belt producer; government recovered $1.2B in mining arrears (2023) |

|

Burkina Faso |

Gold |

Major gold producer; the government nationalized multiple mines (2024-2025) |

|

Nigeria |

Oil, Gas, Tin, Coltan, Iron ore |

37.28 billion barrels of proven oil reserves |

|

Senegal |

Oil, Gas, Gold, Zircon |

New offshore oil production launched in 2024 |

|

Sierra Leone |

Diamonds, Rutile, Bauxite, Iron ore |

World-class alluvial and kimberlite diamonds |

East Africa: The Emerging Frontier

East Africa is the least-exploited mineral region on the continent, which means it is also the region where the next wave of extraction pressure is building. Tanzania is a significant gold producer, with the Geita mine among Africa’s top operations. It also holds nickel, diamonds, and coal. Uganda has announced that a recent geological survey identified gold deposits potentially worth $3 to $5 trillion, though formal reserve certification has not been completed.

Kenya holds significant deposits of titanium, soda ash, and gemstones. Ethiopia is developing gold, platinum, and potash resources. Tanzania and Mozambique have become major offshore gas producers. Madagascar holds graphite, cobalt, nickel, and ilmenite deposits that have attracted growing foreign interest.

|

Country |

Primary Minerals |

Key Facts |

|

Tanzania |

Gold, Diamonds, Coal, Gas, Nickel |

Significant gold producer; major offshore gas fields |

|

Uganda |

Gold, Oil, Iron ore |

Possible $3-5T in gold deposits; 1.7B barrel oil reserves in Lake Albert |

|

Kenya |

Titanium, Soda Ash, Oil |

Turkana oil basin under development |

|

Ethiopia |

Gold, Potash, Platinum, Tantalum |

Emerging producer; potash deposits among the world’s largest |

|

Mozambique |

Gas, Graphite, Titanium, Coal, Ilmenite |

One of the world’s largest undeveloped natural gas reserves |

|

Madagascar |

Graphite, Cobalt, Nickel, Ilmenite |

Significant battery minerals endowment; largely undeveloped |

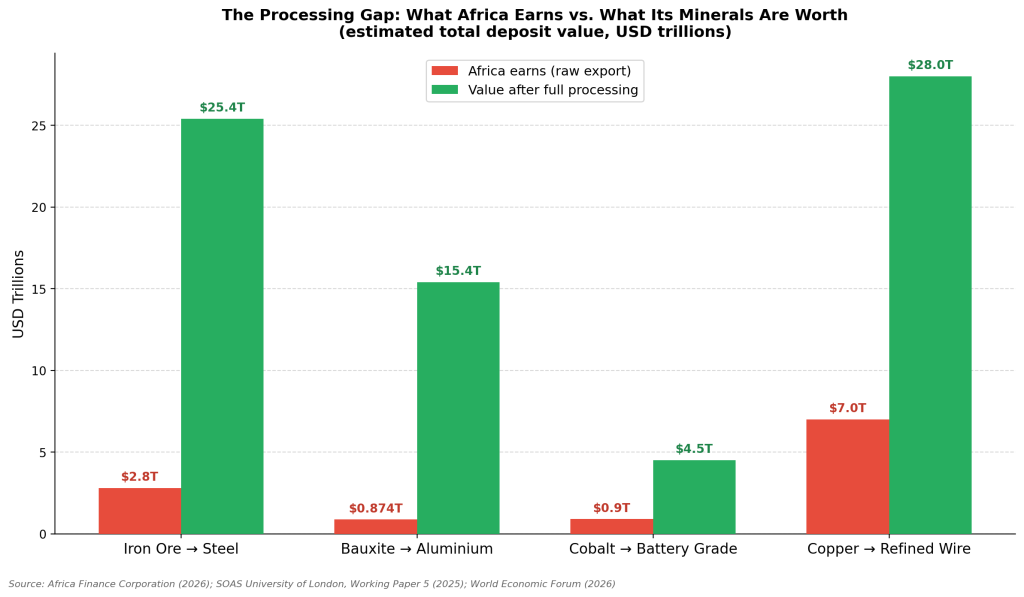

The Processing Gap: Where Africa’s Money Goes

Knowing where the minerals are is only half the equation. The other half is understanding how much money Africa leaves on the table by exporting raw materials instead of processed goods.

The Africa Finance Corporation put it plainly in its 2026 report: Africa effectively pays twice. African producers export on Free on Board terms, paying freight from mine to port. Then finished goods come back on Cost, Insurance and Freight terms, meaning countries pay again to import the processed materials back in. The minerals leave as raw ore. They return as premium products.

The numbers tell the story starkly.

Iron ore worth $2.8 trillion at the mine gate becomes $25.4 trillion once processed into steel. Bauxite worth $874 billion becomes $5.2 trillion as alumina and up to $15.4 trillion as finished aluminum. Cobalt exported as raw concentrate is worth a fraction of battery-grade refined cobalt, with each additional processing stage adding a 15-30% value premium.

Globally, 70% of mining value is created during processing, not during extraction. By missing this stage, Africa loses that majority share of value every single time a ship leaves port loaded with unprocessed ore.

Consider the DRC. It accounts for 76.6% of global mined cobalt yet sends nearly all of it abroad with minimal processing. China, which has been the dominant investor in DRC mines since the mid-2000s, has built out its own domestic processing infrastructure. China controls 73% of global cobalt refining capacity, 40% of copper refining, 59% of lithium processing, and 67% of nickel refining. The DRC mines the cobalt. China refines it. China sells it to manufacturers. Africa does not participate in any of those downstream transactions.

Indonesia understood this and acted. After banning the export of raw nickel ore in 2014, Indonesia grew its total processed nickel export value from $3.1 billion in 2013 to $19.2 billion in 2023. One policy decision, one decade, a sixfold increase in value capture. African policymakers have studied that example closely.

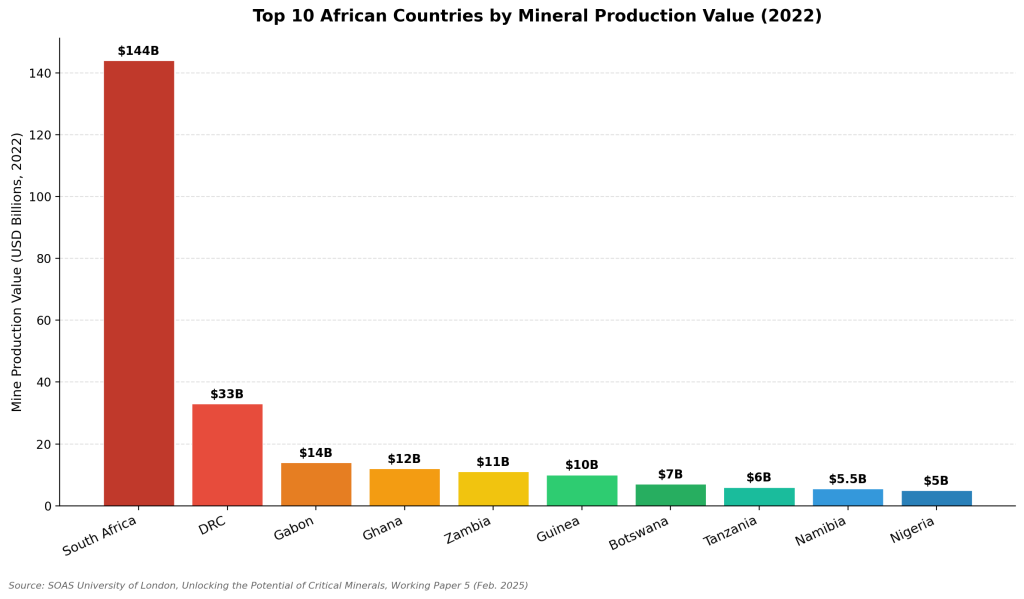

Top Producing Countries: The Hierarchy of Extraction

South Africa leads the continent by a wide margin, producing minerals worth approximately $144 billion in 2022, driven primarily by its platinum group metals, which alone generated $19.7 billion in 2023. The DRC ranks second at $33 billion, driven primarily by copper and cobalt from the Katanga and Lualaba provinces.

This chart also shows how concentrated wealth has become. The top two countries, South Africa and the DRC, account for more than half of the continent’s total mine production value. That concentration is not geological; there are significant deposits across the entire continent. It reflects a century of channeling investment toward specific territories with pre-existing infrastructure, built initially to serve colonial extraction needs.

What Africa Would Earn If Paid Fairly

The concept of “fair” pricing in minerals is not abstract. It has a technical name: the arm’s length principle. Under international tax standards led by the OECD, transactions between related parties, such as a mine in Zambia selling copper to its parent company’s trading hub in Switzerland, should be priced as if the two parties were unrelated. In practice, this principle is routinely violated through a mechanism called transfer mispricing, where the trading hub lowballs the price it pays to the mine, reducing taxable profit in the country where the mineral actually comes out of the ground.

The OECD’s 2023 transfer pricing framework for minerals acknowledged that developing countries face particular challenges: limited access to pricing data, weak tax authority capacity, and contracts that stabilize fiscal terms against any future adjustments. A 2016 Resource Governance study found that Guinea was potentially losing millions of dollars annually because Russian aluminum giant Rusal paid $19 per tonne for bauxite while the international benchmark for comparable ore was $32 per tonne, a $13 per tonne gap on every tonne exported.

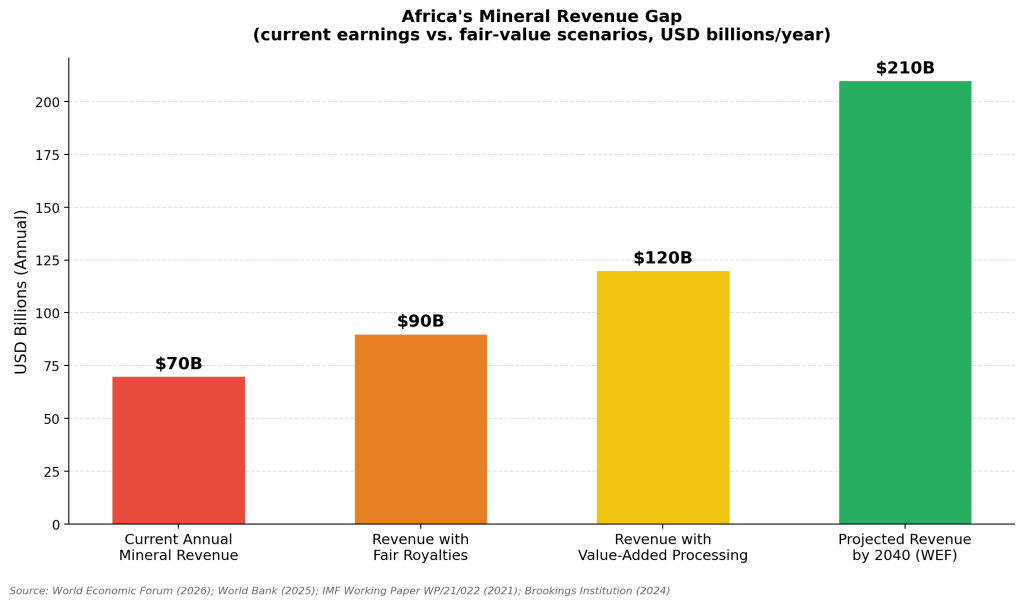

African countries currently collect only about 1% to 3% of their GDP in mining revenue. The World Bank estimates the region misses out on roughly 1.7% of GDP annually in potential tax and royalty income, and that closing the gap with better contracts and stronger fiscal enforcement could unlock up to $20 billion per year in additional government revenue.

If Africa applied fair royalty rates consistently and enforced the arm’s length principle, its annual mineral revenue would rise from roughly $70 billion today to an estimated $90 billion. If African countries processed their key minerals domestically before export, annual revenue could approach $120 billion. The World Economic Forum projects that, with greater value-added processing, Africa’s total mineral market value could reach $210 billion annually by 2040.

These are not utopian projections. They are the result of policy and investment decisions. The decisions have simply been made by others so far.

The Green Energy Transition: A New Leverage Point

There is a factor that did not exist fifty years ago and that changes the negotiating position of every African mineral producer: the global clean energy transition.

Electric vehicles need lithium, cobalt, manganese, and nickel. Solar panels need silicon and silver. Wind turbines need rare earth elements and copper. The IEA projects that by 2050, demand for cobalt could increase by up to 500% from 2020 levels, lithium by nearly 4,300%, and graphite by 2,500%. Africa holds a dominant or major share of most of these minerals.

Revenues from just four minerals, copper, nickel, cobalt, and lithium, are projected to reach $16 trillion globally over the next 25 years. Sub-Saharan Africa is positioned to capture more than 10% of that total. As Brookings Institution analysts concluded, the IEA estimates that by 2040, Africa’s mineral market value could increase by almost three-quarters from today’s $70 billion if the continent captures more of the processing and refining stages.

The world needs what Africa has more than ever before. That is a leverage point. Whether African governments use it will determine whether the next generation of Africans benefits from their own inheritance, or watches it leave through the same port gates their grandparents watched.

Country Profiles: Seven Nations, Seven Stories

Democratic Republic of Congo: The World’s Battery Capital in Poverty

The DRC holds an estimated $24 trillion in untapped mineral wealth. Its cobalt deposits alone are the most strategically important single-country mineral asset on earth for the electric-vehicle era. The country’s 110 million people have a per capita income of under $2 a day. The gap between what is in the ground and what reaches the population is arguably the most extreme case of the resource curse in modern history.

In February 2025, the DRC government imposed a four-month export ban on cobalt, the first major market intervention in the country’s mineral history, to address oversupply that had crashed cobalt prices by 60% since 2022. As of October 2025, the country transitioned to an export quota system capping annual cobalt exports at 96,600 metric tonnes for 2026 and 2027, about half the 2024 export level. At a $ 20-per-pound price, this would raise DRC’s cobalt export value by 24%.

South Africa: Wealth Above and Below Ground

South Africa produces minerals worth more than every other African country combined. Its platinum group metals are experiencing a third consecutive annual supply deficit, with output declining from 5.3 million ounces in 2006 to 3.9 million ounces in 2025. The Bushveld Complex is producing at lower volumes, but at higher prices, as global demand for platinum in hydrogen technology grows.

Despite the production decline, South Africa still supplies approximately 70% of global platinum. Its new Critical Minerals and Metals Strategy of 2025 aims to shift the country from a raw exporter into a value-added supplier.

Zambia: The Copper Nation Fighting for Its Share

Zambia produced 820,000 tonnes of copper in 2024, a 12% increase from the previous year, and is targeting 1 million tonnes in 2025 and 3 million tonnes by 2035. Copper accounts for approximately 70% of Zambia’s export earnings and 12% of GDP. The country earned a record $12.5 billion in copper revenue in 2025.

Zambia’s geological advantage is significant: its copper deposits average 2-3% grade, compared with Chile’s 0.5-0.8%. Yet historically, Zambia has retained only a small fraction of the value of its copper output, through a combination of low royalty rates, negotiated tax concessions, and transfer mispricing through BVI-registered holding structures. The 2024 Minerals Regulations Commission Act and 2025 Local Content Regulations represent the country’s most ambitious attempt to change that equation.

Ghana: The Gold Standard for Reform

Ghana is now Africa’s top gold producer and recorded $20 billion in gold export earnings in 2025, nearly doubling from $10.3 billion in 2024. It replaced the flat 5% royalty on gold with a sliding-scale system ranging from 5% to 12%, tied to global gold prices. At current record gold prices, Ghana collects the maximum 12%. The government also created GoldBod, a state agency that requires large miners to sell up to 20% of their intended gold exports to the state before shipping.

Guinea: The Bauxite Prisoner

Guinea supplies 95% of Africa’s bauxite and is one of the world’s largest exporters. It produces vast quantities of bauxite and earns a fraction of what the mineral is worth as processed aluminum. A 2016 study found that Rusal, the Russian aluminum giant, paid $13 per tonne below international benchmark prices for Guinean bauxite, a gap the government’s tax authority lacked the capacity to challenge effectively. The Intergovernmental Forum on Mining and Metals noted in 2023 that Guinea’s establishment of a bauxite reference price was a significant step toward fairer returns, and a model other African nations are studying.

Botswana: Diamonds and a Deal Under Scrutiny

Botswana is frequently cited as Africa’s minerals management success story. Through the 50-50 joint venture structure of Debswana, the state has captured a larger share of diamond revenue than most African countries capture from any mineral. Botswana’s mining sector consistently delivers over 12% of GDP in government revenue, the highest rate on the continent. De Beers reported Botswana operations contributing 51% more carats in Q3 2025 year-over-year.

However, Botswana’s relationship with De Beers has become more contested. The renegotiated 2023 sales agreement, which was supposed to expand Botswana’s independent selling rights through the state diamond trader, Okavango Diamond Company, contains contract terms that remain under scrutiny. The question of what Botswana is and is not permitted to do with its own diamonds, and to whom it may sell them, will form the basis of Part 2 of this series.

Nigeria: From Raw Exporter to Refining Hub

Nigeria is Africa’s largest oil producer with 37.28 billion barrels in proven reserves, approximately 2.25% of global supply. For most of its post-independence history, Nigeria did what nearly every African resource nation has done: it pumped crude oil out of its ground and shipped it to refineries in Europe and the United States, then paid to import the gasoline, diesel, and jet fuel back. The country exported the raw product at a low value and imported the finished product at a premium, year after year, spending, at one point, as much as $2.6 billion per quarter on fuel imports alone.

That logic has now been directly challenged by one man.

Nigeria’s Dangote Factor

In January 2024, billionaire Aliko Dangote commissioned the Dangote Petroleum Refinery and Petrochemicals complex at the Lekki Free Trade Zone in Lagos, a $20 billion facility that is the largest single-train refinery on earth. At its nameplate capacity of 650,000 barrels per day, it can process enough crude to meet Nigeria’s entire domestic fuel demand, with product left over for export. By February 2026, the refinery had hit full capacity and was supplying approximately 92% of Nigeria’s domestic petrol needs, reducing fuel imports to around 8% of total supply. Nigeria had gone from importing nearly all of its petrol to producing almost all of it domestically in under two years.

The economic effect has been direct and measurable. Nigeria spent $2.6 billion on fuel imports in Q1 2024. In Q1 2025, that figure had fallen to $1.2 billion, a saving of $1.4 billion in a single quarter. The refinery has saved Nigeria an estimated $20 billion in fuel import costs, eased chronic pressure on the naira, and stabilized domestic fuel supply in ways that reduced fuel queue crises that Nigerians had endured for five decades.

Dangote is also now exporting. Between June and July 2025, the refinery exported 1 million tonnes of petrol to countries including Ghana, Cameroon, Togo, Tanzania, and the Ivory Coast, as well as to international markets such as the United States, Oman, Malaysia, and Singapore. Nigeria became, for the first time, a net exporter of refined petroleum products. The refinery additionally produces aviation fuel, diesel, naphtha, polypropylene, polyethylene, and base oil, thereby generating domestic industrial supply chains that previously did not exist.

Dangote has announced plans to expand capacity to 1.4 million barrels per day by 2028, making it the world’s largest refinery by capacity, surpassing India’s Jamnagar complex. The expansion is expected to employ up to 95,000 skilled workers during peak construction. A separate $40 billion investment plan covers further expansion of both the refinery and Dangote’s fertilizer production.

The Dangote refinery is the most concrete single illustration of the processing gap argument in this entire series. Nigeria had the oil all along. The question was never about the resource. It was about who controlled the refining stage and collected the value added there. For decades, that value left Nigeria on tankers. Now, at least in part, it stays.

Nigeria’s non-oil mineral sector, which includes tin, coltan, iron ore, coal, and tantalite, remains substantially underdeveloped. Its 30% Value Addition Bill, currently moving through the legislature, would require at least 30% of raw minerals to be processed domestically before export, applying the same logic Dangote proved in oil to every other mineral the country holds.

The Central Question

The $29.5 trillion figure is an inventory, not a guarantee. It says what exists. It does not say who will benefit from it.

Every mineral extraction deal is, at its core, a question about sovereignty: who controls the terms under which a country’s irreplaceable, non-renewable natural wealth leaves its soil. For most of the 20th century, those terms were written in European capitals and enforced through colonial legal structures that evolved into corporate legal structures without losing their essential function.

The question for the 21st century is whether the governments of the continent, and the citizens they represent, have both the legal tools and the political will to write different terms. The resources exist. The leverage exists, arguably more than at any previous point in history, because the world’s clean energy transition is wholly dependent on African minerals. What has often been missing is the institutional capacity to enforce a fair return and to protect against foreign interference when governments try.

In Part 2, we examine one country, one mineral, and one contract in detail: Botswana, diamonds, and the De Beers sales agreement.

Sources

This report draws on the following primary and secondary sources. All figures are in U.S. dollars. Production and reserve data reflect the most recent available year, generally 2024 or 2025.

- Africa Finance Corporation. (2026). Compendium of Africa’s Strategic Minerals: A $29.5 Trillion Endowment. africafc.org.

- World Economic Forum. (April 2026). “Africa’s Critical Minerals and the Energy Transition.” weforum.org.

- International Monetary Fund. (2021). “Base Erosion, Profit Shifting and Developing Countries.” IMF Working Paper WP/21/022. elibrary.imf.org.

- World Bank. (2025). “Africa’s Untapped Natural Resource Potential.” blogs.worldbank.org.

- U.S. Geological Survey. (2025). Mineral Commodity Summaries 2025. usgs.gov.

- Organization for Economic Co-operation and Development. (2023). Determining the Price of Minerals: A Transfer Pricing Framework. oecd.org.

- Zero Carbon Analytics. (2024). “Developing Africa’s Mineral Resources: What Needs to Happen.” zerocarbon-analytics.org.

- SOAS University of London. (February 2025). “Unlocking the Potential of Critical Minerals.” Working Paper 5. soas.ac.uk.

- Natural Resources Canada. (2024). “Cobalt Facts.” natural-resources.canada.ca.

- Resource Governance Institute. (2016). “Transfer Pricing in Mining: Orientation for the Development Community.” resourcegovernance.org.

- Ghana Gold Board (GoldBod). (2025). “Ghana Records US$20bn in Gold Export Earnings in 2025.” goldbod.gov.gh.

- Friends of the Congo. “Congo’s Minerals.” friendsofthecongo.org.

- African Business. (September 2024). “Dangote Refinery: Adding Value to Nigeria’s Crude.” African Business.

- Economic Confidential. (2025). “Dangote Refinery Saves Nigeria $20 Billion in Fuel Import Costs.” economicconfidential.com.

- The Nation Nigeria. (2025). “Dangote Refinery Saves Nigeria N10bn Annually.” thenationonlineng.net.

- Intergovernmental Forum on Mining, Minerals, Metals and Sustainable Development. (2023). “Guinea Bauxite Reference Price.” igfmining.org.

- Brookings Institution. (2024). “Unlocking Africa’s Critical Minerals for Broad-Based Prosperity.” brookings.edu.

- IEA. (2023). Critical Minerals Market Review 2023. iea.org.

- Africa Practice. (2024). “When the Rules Break: Closing Africa’s Mineral Value Gap.” africapractice.com.

- B20 South Africa. (November 2025). Africa at the Core of Critical Minerals. b20southafrica.org.

- J.P. Morgan Private Bank. (June 2024). “Global Race for Critical Minerals: A Unique Opportunity for Latin America.” privatebank.jpmorgan.com.

- Minerals Council of Australia. (2021). Best in Class: Australia’s Bulk Commodity Giants. minerals.org.au.

- New Lines Institute. (March 2024). “The Race for Rare Earth Minerals.” newlinesinstitute.org.

- Al Jazeera. (February 15, 2022). “Mapping Africa’s Natural Resources.” aljazeera.com.

- Stimson Center. (February 2025). “Competing for Africa’s Resources: How the U.S. and China Invest in Critical Minerals.” stimson.org.

- African Energy Chamber. (January 2026). State of African Energy 2026 Outlook. energychamber.org.

The Africana Voice is an independent publication covering African affairs for readers in the diaspora, on the continent, and in Kenya. Research for this report was powered by Perplexity.

LEAVE A COMMENT

You must be logged in to post a comment.